Illustrative image (Source: cafef.vn)

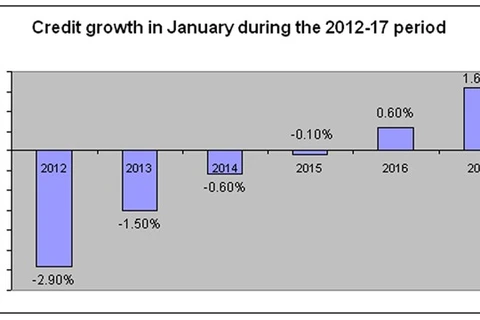

Illustrative image (Source: cafef.vn) Hanoi (VNA) - Credit growth in the first two months of 2017 rose 1.23 percent year-on-year, but credit institutions remain cautious over business targets while focusing on lending quality.

The growth seen in 2017 was higher than the 0.33 per cent growth rate noted in the first two months of 2016, according to a report from the Ministry of Planning and Investment.

Industry insiders said the rise in the first months of the year would help credit growth spread more evenly across each quarter instead of only making an impact in the last quarter, as in previous years.

According to expert Nguyen Tri Hieu, based on the current condition of the global economy, optimistic forecasts of the country’s credit growth for this year can still be maintained.

However, he added, the rise for two months alone cannot say much, as there could be many fluctuations, especially in imports and exports, in the remaining months of the year. "If the world economy experiences a strong shake-up, this will surely affect Vietnam," he said.

Credit institutions also appear cautious with their business goals as they have set lower credit growth targets this year than last year. Vietcombank, for example, has set a credit growth target of roughly 18 percent this year, lower than the 18.9 percent rise seen last year.

In discussing the caution being exercised by credit institutions, experts have said there are both domestic and international causes behind it.

According to experts, the global economy in 2017 is forecast to be challenging and will have an impact on Vietnam’s economy, which is wide open and dependent on exports.

Now, even the US government is moving towards trade protectionism, bringing US manufacturers back to the US market. The US’s economic relations with other nations are also under review. This will partly reduce foreign investment in Vietnam, as investors tend to return to traditional markets when the global economy slows down.

Banks seem to have acknowledged this risk too, so they are being more cautious with their business goals, the experts forecast.

In the domestic market, the State Bank of Vietnam (SBV) has claimed it will continue to apply tight controls over lending in potentially risky areas, such as lending to large clients, real estate, and BOT and BT projects in the transport sector.

Under SBV’s Circular 06/2016/TT-NHNN on asset-liability management and real estate loans, commercial banks have been allowed to use a maximum ratio of 50 percent short-term funding for loans with terms extending beyond 12 months since the end of 2016, down from the previous 60 percent. This ratio will be reduced to 40 percent by the end of 2017.

Circular 06 also raised the risk weights for real estate loans to 200 percent from the end of 2016, from the previous 150 percent.

The rising risk weight means if commercial banks want to expand their real estate loans segment, they must increase their capital to have a capital adequacy ratio of at least 9 percent. If they fail to increase their capital, the banks must limit their scale of lending. Meanwhile, it remains difficult to raise capital at this time.

Besides, many commercial banks have also prioritised the quality of lending instead of only focusing on credit growth as previously.

Pham Hong Hai, General Director of HSBC Vietnam, told Thoi bao ngan hang (Banking Times) that credit flows should focus on key areas of the economy, based on the effective measurement of capital flow. Hai also agreed with the central bank’s decision to tightly control the amount of capital pouring into potentially risky areas, such as real estate and securities.

According to Hai, if credit growth is too high, banks will face many difficulties in maintaining and ensuring the security of their capital in future.

Nghiem Xuan Thanh, Chairman of Vietcombank, which was the first bank to successfully recover all bad debts sold to the Vietnam Asset Management Company and currently has a bad debt ratio of less than 1.5 percent, said his bank planned to actively promote lending to the government’s five priority areas this year.

Outstanding loans to these areas amounted to 170 trillion VND (7.49 billion USD), accounting for 35 percent of the bank’s total outstanding loans. The priority areas include agriculture and rural development, production for export, small and medium enterprises, support industry and hi-tech application.

Expert Hieu said the most important task for banks in using their capital effectively is to manage risk, adding that banks should only provide loans to well-scrutinised applicants. The governance of banks must also be changed to fit reality.

In addition, operating costs must be considered, the expert said.-VNA

VNA