Manufacturing and services sectors are likely to recover and be the main growth driver in the second half of the year (Photo: vcci.com.vn)

Manufacturing and services sectors are likely to recover and be the main growth driver in the second half of the year (Photo: vcci.com.vn) HCM City (VNA) - Standard Chartered Bank expects Vietnam’s growth to slow to a multi-year low of 3 percent this year on soft external demand, with external headwinds set to offset domestic outperformance.

The forecast is in the bank’s recently published research report for the third quarter.

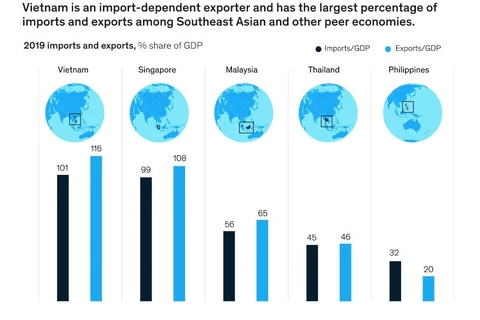

“Growth is likely to rebound in the second half of the year (H2) driven by the strength of the domestic economy; global headwinds are likely to partially offset this. Vietnam’s dependence on the global economy is the second-highest in ASEAN after Singapore; its trade-to-GDP ratio of 198 percent is among Asia’s highest, driven by electronics exports. We expect 3 percent growth in Vietnam in 2020; further monetary and fiscal support in H2 could push growth closer to the Government’s target of 4-5 percent,” said Chidu Narayanan, economist for Asia, Standard Chartered Bank.

According to the latest macro-economic report, manufacturing and services sectors are likely to recover and be the main growth driver in the second half of the year. The manufacturing sector growth is estimated at roughly 1.5 percent in 2020, with its contribution to growth down 1.8 percentage points. The services sector’s contribution to growth is likely to fall to 0.5 percentage points from 2.8 percentage points in 2019.

Construction activity is expected to decline on subdued sentiment and declining foreign direct investment (FDI). However, public infrastructure investment is likely to be stronger than in the past 18 months, driven by Government stimulus. A slowdown in tourism and related activities is likely to weigh on consumption, which is projected to pick up in H2 following the reopening of the economy but to remain below 2019 levels.

Standard Chartered’s economists anticipate Vietnam’s trade to pick up in H2 as global demand recovers, but a recovery to pre-COVID levels is unlikely. Demand from China should support a pick-up in both exports and imports near-term; however, subdued global demand is likely to impact trade growth. The bank expects trade balance to remain in surplus this year as lower imports offset soft exports.

The study forecasts FDI inflows to decline this year on heightened uncertainty and depressed investment sentiment globally, totalling 13 billion USD. Government measures should support FDI inflows in H2.

In addition, the sustained relocation of low-tech manufacturing to Vietnam amid geopolitical tensions should partly offset subdued sentiment, supporting FDI inflows./.

VNA