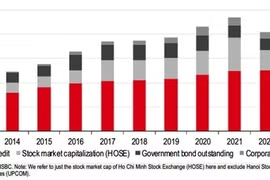

Hanoi (VNA) - Thanks to the AI boom, tech-exposed economies like Vietnam, Singapore, and Malaysia are better positioned in trade, according to a recent report by HSBC.

In its report titled “ASEAN Perspectives: Whoever gets the chips rules the trade,” HSBC Global Investment Research said the Middle East conflict is an acute reminder of how sensitive fast-growing ASEAN is to high energy costs given its reliance on energy imports.

While it is important not to overlook high energy costs, it is also vital not to be distracted by near-term energy volatility and return to ASEAN’s growth fundamentals. One key pocket of resilience is ASEAN’s central position in the global tech supply chain, enabling the regional economies to ride the AI wave. Unsurprisingly, the 2025 regional growth outperformers all have heavy exposure to the tech industry, the research shows.

But not everyone benefits to the same extent. Singapore is in the best position to capture the AI boom, given its prominence in the high-end memory chip space. The next big beneficiary is Malaysia, with its electronics powerhouse in Penang, which has grown its market share in logic chips like processor and amplifier chips.

Vietnam has taken a different path, growing impressively in the consumer electronics segment, but also with an ambition to climb up the value chain further.

Recent US-China trade tensions have pushed the region to embed further into the global tech supply chain, strengthening their positions in this strategic sector.

But not everyone benefits to the same extent: those economies with an extensive tech supply chain are riding on the tech wave. Electronics exports in Malaysia and Vietnam, measured as a percentage of GDP, highlight the weight of tech exports in their respective economies. Elsewhere, electronics non-oil domestic exports (NODX), despite only accounting for 8% of Singapore’s GDP, also benefits the Lion City for related sectors like precision engineering and wholesale trade services.

The tech beneficiaries – Vietnam, Malaysia and Singapore – stood out in their 2025 GDP performances. While it is not all driven by trade (their domestic resilience cannot be underestimated), the AI-driven tech upcycle has nonetheless been supportive. Growth in all of them in 2025 well exceeded their respective average in the past decade.

When Singapore and Malaysia are leading ASEAN in their semiconductor exports, Vietnam is choosing a different path: it has elevated its importance in final electronics assembly, specialising in finished consumer electronics, thanks to supply chain diversification from tech MNCs like Samsung.

Vietnam’s share of consumer electronics, including smartphone, printers and computers, has seen a notable jump from almost none to 8-15% in 15 years. Besides consumer electronics, Vietnam also strives to climb up the value chain, targeting the IC segment. However, unlike Singapore and Malaysia, it has seen a dwindling share of global processor chips, despite billions of dollars of investment from Intel.

Despite the positive outlook, HSBC experts noted that economies such as Vietnam also face considerable risks.

If high energy prices persist for long, the second-round effect is likely to ultimately affect AI-driven tech demand. In addition, the fate of potential tariffs on semiconductors continues to be the region’s Sword of Damocles, leaving a risk that tech-exposed economies could become the victims of their own success.