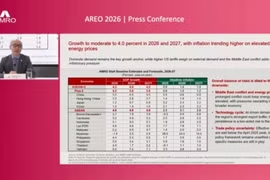

Jakarta (VNA) – Economic growth across the ASEAN+3 region is expected to slow to about 4% in 2026 and 2027 as escalating geopolitical tensions, energy disruptions, and global trade uncertainty weigh on the outlook, according to the ASEAN+3 Macroeconomic Research Office (AMRO).

Speaking at a recent session titled "ASEAN Regional Economic Outlook and Fiscal Policy" in Yogyakarta, Indonesia, AMRO Senior Economist Catharine Kho warned that the region's economic outlook remains uncertain, with inflation potentially rising due to the impact of conflicts in the Middle East, global tariff developments, and changes in the global technology cycle.

The economist held that tensions in the Middle East are currently the biggest risk to the region's economy due to their direct impact on global energy supply and prices.

AMRO stated that the current energy supply disruptions are the most severe in decades, elaborating that the scale of disruption is four times larger than what the world experienced during the Russia – Ukraine conflict in 2022.

World oil prices could exceed 100 USD per barrel if the conflict spreads further across the region, potentially pushing ASEAN+3 inflation to around 2.2%, according to the organisation's analysis.

However, AMRO assessed that the ASEAN+3 economies, which consist of 11 ASEAN member states, China, Japan and the Republic of Korea, will maintain resilience in 2025 thanks to stable domestic demand, low inflation, continued investment inflows, and robust exports driven by artificial intelligence-related semiconductor demand.

AMRO noted Asia is no longer merely the “factory of the world” but is gradually becoming a major consumer market. It estimated that the ASEAN+3 region now accounts for 28% of total global final demand, exceeding the size of the US consumer market.

For Indonesia, ASEAN+3 economies account for nearly 60% of its exports, underscoring the country’s growing dependence on regional trade linkages.

In the context of continued global economic volatility, AMRO recommended governments maintain policy flexibility while preserving fiscal and monetary buffers to respond to future shocks./.